Absorption Costing Explained, With Pros and Cons and Example

Many accountants claim that administrative, fixed manufacturing, and marketing and distribution overheads are period costs. They have little long-term credit note wikipedia value and therefore should avoid including in the product’s pricing. Companies with a consistent demand for products benefits from absorption costing.

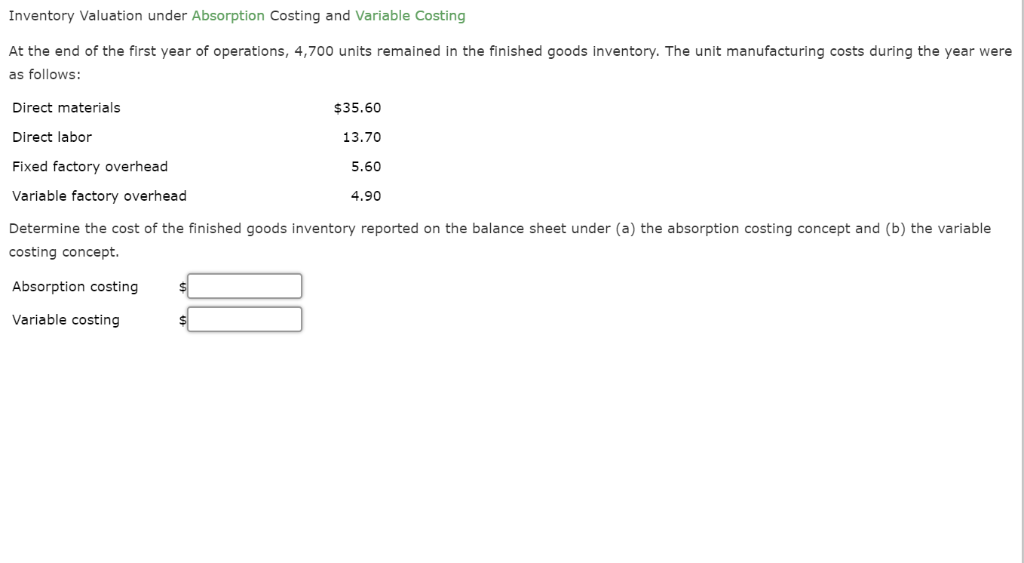

Calculating Ending Inventory Using Absorption Costing

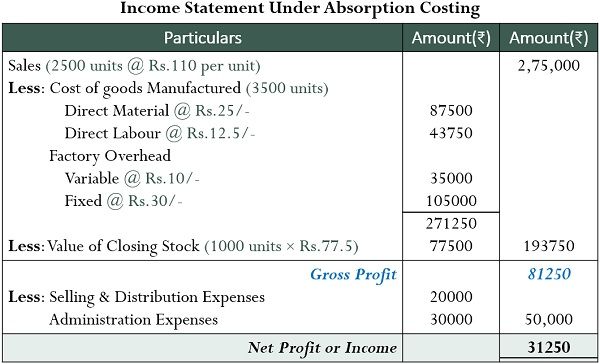

This is an excellent method for the absorption of overhead costs in industries where much of the work is performed with the help of machines. Under this method, total direct labor hours are used to determine the overhead absorption rate. Absorbed cost calculations produce a higher net income figure than variable cost calculations because more expenses are accounted for in unsold products, which reduces actual expenses reported.

Create a Free Account and Ask Any Financial Question

As 8,000 widgets were sold, the total cost of goods sold is $56,000 ($7 total cost per unit × 8,000 widgets sold). The ending inventory will include $14,000 worth of widgets ($7 total cost per unit × 2,000 widgets still in ending inventory). Indirect costs are those costs that cannot be directly traced to a specific product or service.

What Not to Include in an Absorption Costing System

Overhead absorption is defined as the allotment of overheads to cost units. When the amount of overheads has been determined on the predetermined basis for each cost center, the next step is to charge it to production. Let’s walk through an example of absorption costing to illustrate how it works. Suppose we have a fictional company called XYZ Manufacturing that produces a single product, Widget X. This includes the cost of all materials that are directly used in the manufacturing process.

- In summary, absorption costing principles provide businesses with an accurate, GAAP-compliant accounting method to incrementally track product profitability changes tied to production volumes.

- General or common overhead costs like rent, heating, electricity are incurred as a whole item by the company are called Fixed Manufacturing Overhead.

- Ideally, the quantity and cost of materials in each product are uniform, and processing is also uniform.

- Thus, the absorption of overheads is the function of apportioning overhead costs to individual units, jobs, production lots, processes, work-orders, or such other convenient cost units.

The assignment of costs to cost pools is comprised of a standard set of accounts that are always included in cost pools, and which should rarely be changed. The steps required to complete a periodic assignment of costs to produced goods is noted below. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network.

Is Variable Costing More Useful Than Absorption Costing?

Finance Strategists has an advertising relationship with some of the companies included on this website. We may earn a commission when you click on a link or make a purchase through the links on our site. All of our content is based on objective analysis, and the opinions are our own. If, however, it falls short of the actual overhead, the difference is known as under-applied overhead. The product of this calculation will indicate the amount of overhead to be applied (or charged) to production for the period.

This enables businesses to make informed decisions and maintain accurate financial records in a complex manufacturing environment. It further makes it a useful tool for evaluating suitable product pricing. (b) Each component of the product should bear its own share of the total cost.

Absorption costing has some limitations, and it can be challenging to assess the impact of changes in production levels on profitability since fixed overhead costs remain constant. Operating expenses are represented on the income statement in the same way under absorption and variable costing. Both fixed and variable operating expenses incurred during the period are recorded. The overhead absorption rate is an important concept in management accounting. It helps companies determine the full cost of producing a product or service.